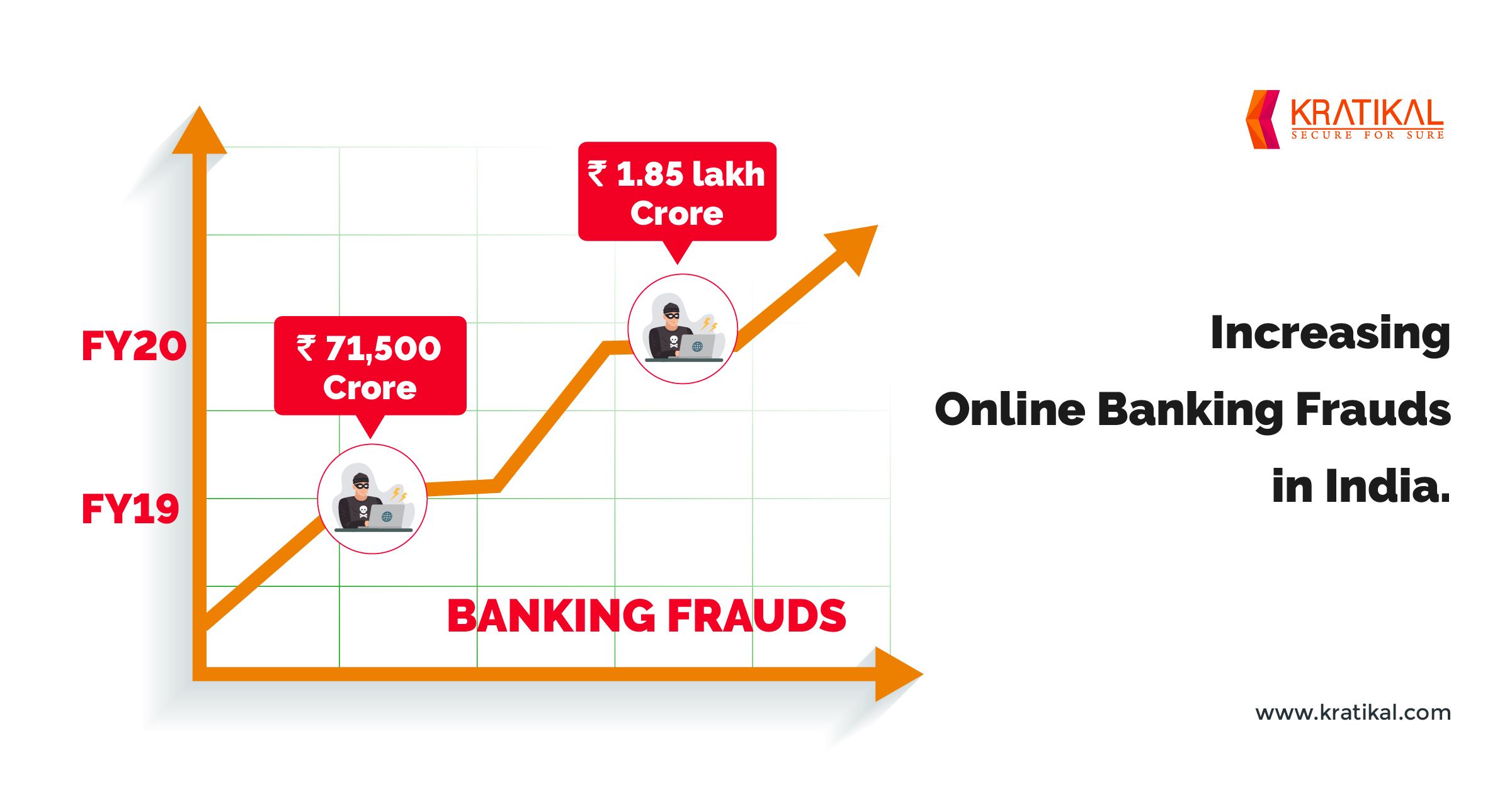

Recent data released by the Reserve Bank of India highlights a concerning trend in India’s financial system: the total amount involved in banking frauds has increased sharply, even as the number of reported fraud cases has declined.

This paradox points towards fewer but larger-value frauds, raising serious concerns about corporate governance, regulatory oversight, and systemic risk in the banking sector.

Understanding the Trend

According to regulatory assessments:

-

The number of fraud cases has reduced due to better reporting standards and early detection of small frauds

-

However, the value of frauds has surged, driven largely by:

-

Large corporate loan defaults

-

Complex financial manipulation

-

Delayed recognition of stress

-

This indicates a shift from petty frauds to high-value, high-impact frauds.

Why Is the Fraud Amount Increasing?

Several structural and institutional factors explain this trend:

1. Large Corporate Frauds

A small number of corporate accounts account for a disproportionately large share of fraud value, often detected years after the actual wrongdoing.

2. Delayed Detection

Frauds are frequently classified only after loans turn into NPAs, by which time the amount involved has already ballooned.

3. Complex Financial Structures

Layered transactions, shell companies, and regulatory arbitrage make detection difficult.

4. Governance Failures

Weak internal controls, poor risk assessment, and lack of accountability in some banks exacerbate the problem.

Role of Digitalisation

While digital banking has improved efficiency, it has also introduced new vulnerabilities:

-

Sophisticated cyber-enabled frauds

-

Phishing and identity theft

-

Mule accounts facilitating fund diversion

However, most of the value-heavy frauds still originate from loan-related activities, not retail digital frauds.

Economic and Financial Implications

The surge in fraud amount has wider consequences:

-

Erosion of public trust in banks

-

Higher fiscal burden due to recapitalisation of public sector banks

-

Reduced credit availability to productive sectors

-

Threat to overall financial stability

Ultimately, banking frauds impose hidden costs on taxpayers and honest borrowers.

Regulatory and Policy Measures

The RBI and government have initiated multiple reforms:

-

Strengthening early warning systems (EWS)

-

Enhanced forensic audits

-

Improved coordination with investigative agencies

-

Stricter norms for large borrowers

-

Use of data analytics and AI in fraud detection

Yet, prevention remains more effective than post-facto punishment.

Way Forward

To address the rising value of frauds, India needs to:

-

Strengthen corporate governance and accountability

-

Improve real-time monitoring of large exposures

-

Reduce delays in fraud classification

-

Enhance bank staff training in risk management

-

Ensure faster legal resolution and recovery

A culture of risk awareness and transparency is crucial.

Relevance for UPSC & State PCS Aspirants

This topic is important for:

-

GS Paper III (Economy & Banking)

-

Essay (Financial Integrity & Governance)

-

Interview questions on banking reforms

Key answer dimensions:

-

NPA–fraud linkage

-

Regulatory gaps

-

Technology vs governance

Conclusion

The rise in the amount of banking fraud despite fewer cases underscores a deeper structural issue within India’s financial system. While regulatory vigilance has improved, tackling large-value frauds requires stronger governance, faster detection, and uncompromising accountability.

Ensuring banking integrity is not just a financial necessity—it is a cornerstone of economic stability and public trust.